18 Jun 2026

Inside the Mechanics of Instant Settlement Processes for Independent Retailers Handling Daily Cash Flow Needs

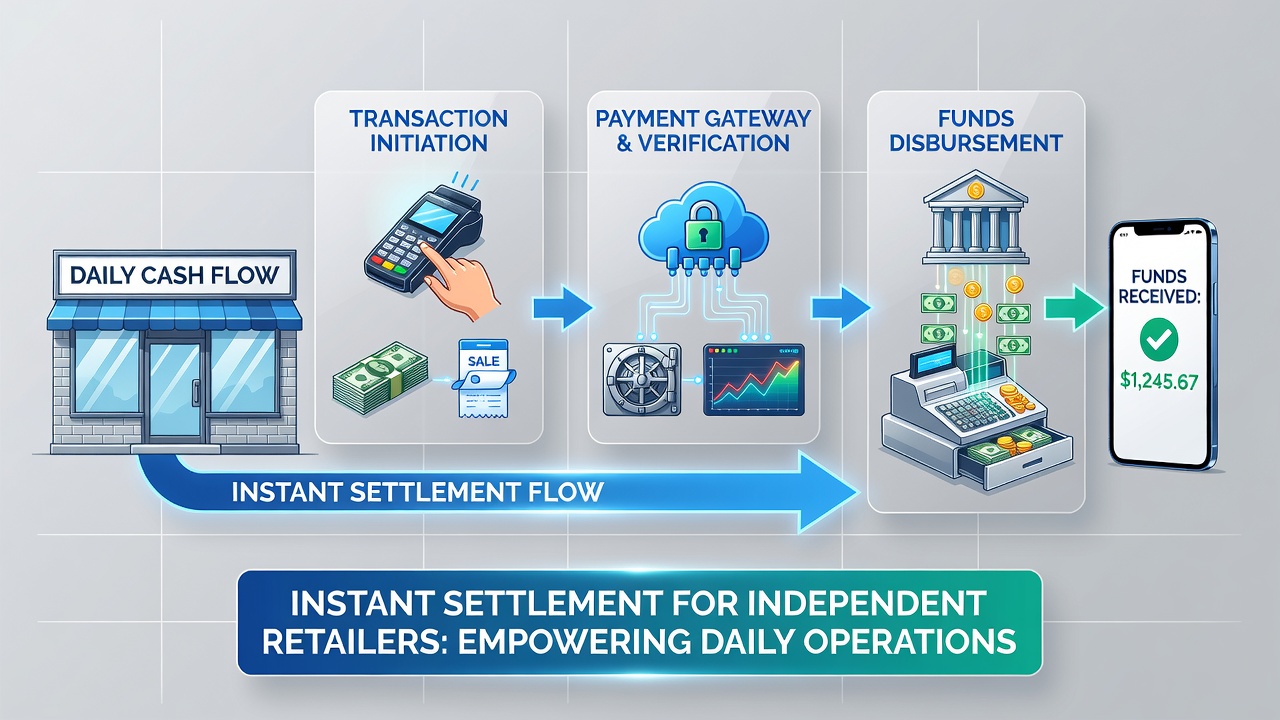

Independent retailers often rely on instant settlement mechanisms to move funds from customer payments directly into their accounts within minutes rather than waiting for traditional batch processing cycles that can stretch across one or two business days. These systems operate through coordinated networks involving payment processors, acquiring banks, and card networks that verify authorization and trigger immediate fund transfers once a transaction clears initial checks.

Core Components of Instant Settlement Systems

Payment gateways communicate with card issuers in real time to confirm available funds while simultaneously flagging the transaction for instant credit to the merchant account. Data flows from the retail terminal through encrypted channels to the processor, which then interfaces with the card network to complete authorization, and at that point the settlement instruction routes to the acquiring bank for immediate credit. Observers note that this sequence reduces the float period dramatically compared with end-of-day batch submissions where funds sit pending until the next clearing window opens.

Independent operators track these movements through dashboards that display pending credits alongside actual bank ledger updates, allowing precise monitoring of available balances for inventory purchases or payroll obligations. Research from payment industry reports indicates that retailers using instant options experience faster reconciliation cycles because transaction records post simultaneously on both merchant and bank sides.

Impact on Daily Cash Flow Management

Small retail locations handling high volumes of card payments benefit when settlements arrive the same day rather than the following morning, since suppliers often demand payment on delivery for perishable stock or promotional items. Cash flow statements prepared at close of business therefore reflect actual rather than projected deposits, which supports more accurate forecasting models used by accounting software. Figures from the European Central Bank show rising adoption of instant credit facilities among smaller merchants across several member states as these tools integrate with standard point-of-sale hardware.

Merchants who previously maintained reserve balances to cover timing gaps now allocate those reserves toward expansion or debt reduction once settlement speed increases. The process also interacts with automated inventory tools because updated sales data triggers reorder alerts without waiting for funds confirmation from slower batch systems.

Technical Pathways and Network Coordination

Settlement instructions travel across rails such as the Faster Payments Service in the United Kingdom or similar real-time systems operated by central banks in other regions, where messages carry both authorization details and credit directives in a single packet. Processors embed risk parameters that allow low-value or previously approved merchant transactions to bypass secondary review queues, which shortens the overall timeline from swipe to bank credit. Those who manage these integrations report that API connections between the payment terminal software and the bank ledger must maintain continuous uptime to avoid dropped instructions during peak hours.

Data from the Federal Reserve highlights continued expansion of same-day settlement options for card transactions in the United States, with participating institutions required to meet specific operational standards for message formatting and exception handling. Independent retailers connect through their chosen acquirer rather than directly to these networks, yet the underlying protocols determine whether a transaction qualifies for instant treatment or defaults to next-day processing.

Operational Considerations for Retailers

Staff training covers how to interpret settlement status codes on terminals so that discrepancies can be flagged before they affect daily totals. Many locations run parallel reports that compare card network confirmations against bank statements to verify that instant credits have posted correctly. When volume spikes occur around seasonal events, the same systems maintain throughput because they segment high-priority transactions for accelerated routing while lower-value ones follow standard instant queues.

Retailers also examine fee structures attached to instant options because some processors apply surcharges that offset part of the cash-flow advantage. Comparisons across providers reveal differences in cutoff times and supported card types, prompting operators to select arrangements that align with their typical transaction mix and supplier payment schedules.

Developments Expected by Mid-2026

By June 2026 several central banks plan to expand eligibility criteria for instant settlement participation, allowing a broader range of smaller acquirers to offer the service without requiring direct network membership. Updated message standards scheduled for rollout will include additional data fields for invoice references, which should improve automated matching between sales records and bank deposits. Industry analyses project that these changes will reduce exception rates further as reconciliation tools gain access to richer transaction metadata.

Conclusion

Instant settlement processes continue to reshape cash management practices for independent retailers by shortening the interval between customer payment and available funds. The mechanics rely on synchronized communication among terminals, processors, networks, and banks, supported by real-time rails operated under regulatory frameworks in multiple jurisdictions. Retailers who implement these options gain clearer visibility into daily balances while maintaining compatibility with existing inventory and accounting systems. Ongoing network enhancements scheduled through 2026 aim to widen access and refine data exchange standards, providing additional precision for operations that depend on predictable daily inflows.