7 Jun 2026

Pathways of Information Between Portable Payment Units and Financial Institutions in Times of Increased Commercial Volume

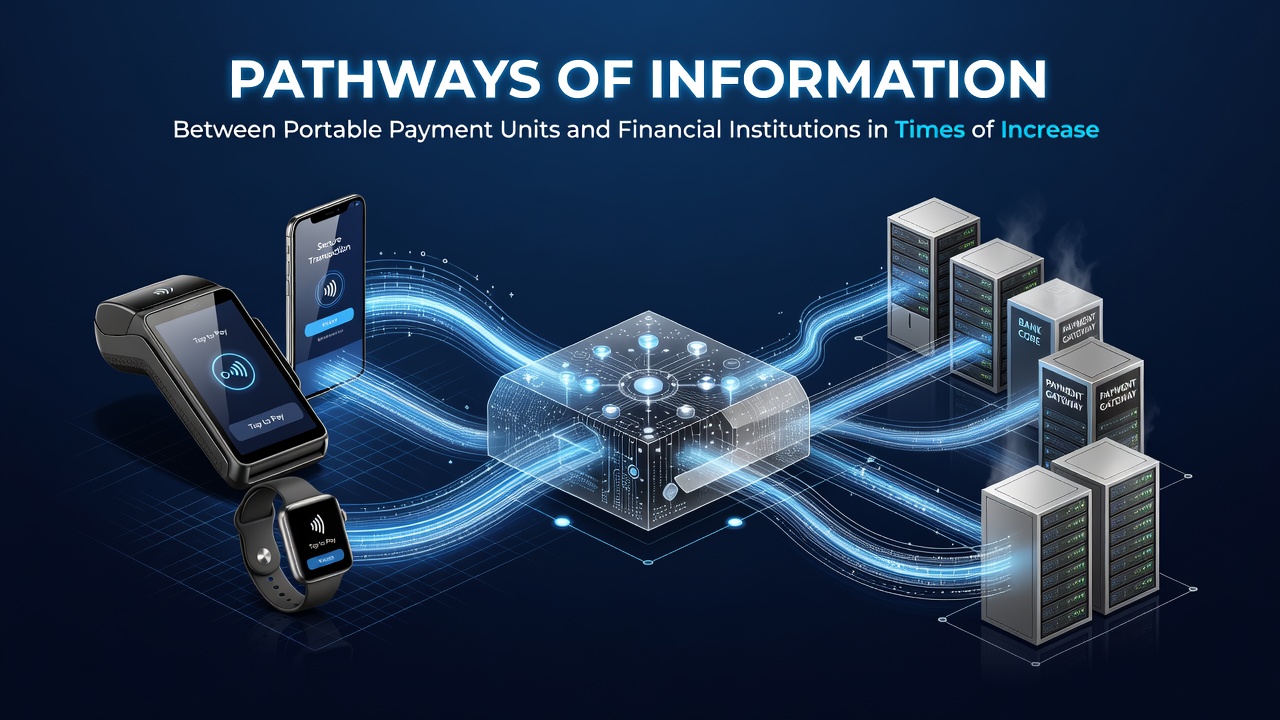

Portable payment units transmit transaction details through layered networks that connect merchants directly to financial institutions, and these pathways expand significantly when commercial activity rises. Data moves from handheld terminals or mobile devices to acquirer banks via encrypted channels, then routes through payment card networks before reaching card issuers for authorization decisions.

Observers note that the process begins at the device level where card or contactless information gets captured and formatted into standardized messages. These messages travel over cellular or Wi-Fi connections to payment processors, which validate format and initiate routing sequences. During peak periods such as summer retail surges leading into June 2026, volume increases require additional bandwidth allocation across these same routes to maintain response times under two seconds for most authorizations.

Core Transmission Routes and Network Layers

Information follows established protocols that include ISO 8583 messaging standards for card transactions and newer formats supporting real-time payments. Portable units send requests containing merchant identifiers, transaction amounts, and cryptographic tokens through secure sockets to gateway servers operated by processors. Those servers forward the data to card networks including VisaNet and Mastercard Network, which apply routing rules based on issuer identification numbers before delivering packets to the appropriate financial institution systems.

Research indicates that satellite or backup terrestrial links activate when primary mobile networks experience congestion, and this redundancy becomes critical when transaction counts multiply during holiday seasons or promotional events. Financial institutions receive the authorization request, check account balances and fraud indicators, then return approval or decline codes along the reverse pathway within milliseconds.

Volume Scaling Mechanisms in Mid-2026 Retail Cycles

By June 2026 data from the European Central Bank showed elevated mobile point-of-sale activity across European markets during seasonal sales, with portable device usage rising in outdoor markets and temporary retail setups. Systems scale capacity through load balancers that distribute incoming messages across multiple processing nodes while preserving message sequence integrity. Observers note that tokenization replaces actual card numbers at the device or gateway stage, reducing sensitive data exposure as volume climbs.

Payment processors monitor queue depths and automatically adjust routing priorities to prevent bottlenecks. When commercial volume spikes, institutions often deploy additional virtual instances of authorization engines, allowing pathways to handle several times the baseline throughput without altering the underlying message formats or security layers.

Security and Compliance Along the Pathways

Encryption standards such as TLS 1.3 protect data in transit between portable units and financial endpoints, while end-to-end tokenization further segments sensitive elements. Financial institutions apply real-time risk scoring at the point where messages arrive from card networks, and any flagged transactions trigger additional verification steps before final responses travel back. According to Federal Reserve payment system documentation, these layered controls operate continuously regardless of transaction volume.

Portable units themselves perform initial encryption and key rotation locally, then transmit only the protected payloads. Institutions maintain audit logs that record every hop along the pathway, enabling post-transaction reconciliation during high-volume periods when thousands of messages per minute cross the same infrastructure.

Intermediary Roles and Real-Time Adjustments

Processors and switches function as intermediaries that translate between device-specific formats and institution-readable messages. During increased commercial activity these entities apply dynamic throttling to smooth traffic spikes, ensuring that no single pathway becomes overwhelmed. Researchers at institutions studying payment infrastructure have documented how failover mechanisms reroute traffic to alternate data centers when primary connections slow under load.

Portable payment units often cache transaction records locally when connectivity drops momentarily, then forward the accumulated data once pathways reopen. Financial institutions receive these delayed batches and process them in sequence while continuing to handle live requests, maintaining overall system stability even as total volume remains elevated.

Conclusion

Pathways between portable payment units and financial institutions rely on standardized messaging, layered encryption, and scalable routing to manage information flow during periods of heightened commercial activity. Data travels through devices, processors, networks, and issuers in coordinated sequences that adapt to volume changes through automated capacity adjustments and redundant connections. Records from June 2026 illustrate how these established routes accommodate rising transaction counts while preserving authorization speed and security requirements across multiple regions.